Economics Design

Financial risk exposures for stablecoins arise from multiple sources including asset collateral, external governance and the ability of token in maintaining at its pegged price. Given the complexity of these issues and the different characteristics of each type of stablecoins, it is often difficult to compare the level of financial risk exposures between tokens. A possible approach here is to develop a system of risk ratings that cover the various aspects of potential sources of risk, and assign each token a risk score based on the applicable parts. In this article, we will walk through the metrics considered, and give an example of how the ratings system can be used to conduct cross-token analysis for a group of stablecoins.

The risk rating system works in a similar way to credit rating systems used in traditional financial analysis. The main areas being covered are collateral health (with accommodations for different types of collaterals), external governance and ability of price peg maintenance. The cutting point between each level is chosen based on analysis results on empirical token prices.

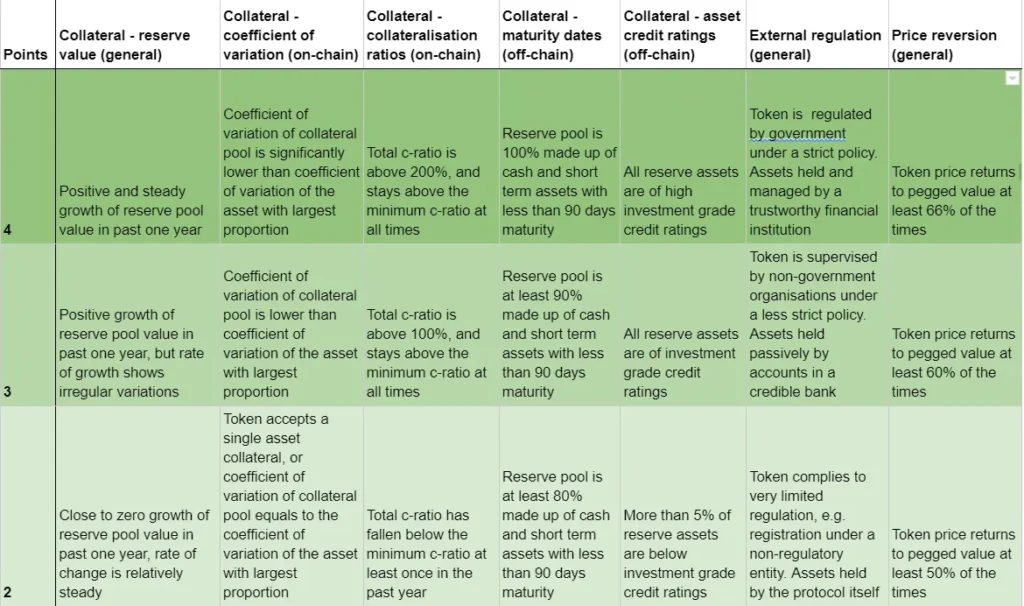

Table 1. Financial risk rating system

Collateral (general) – growth of reserve value

The value of reserve or collateral pool is an important indicator of whether the stablecoin is financially healthy. Growth in collateral pool value can be due to increasing amount of assets being deposited, hinting there are more investors interested in holding to their tokens, or due to the increase in prices of underlying assets which prevents loss from forced liquidations. For a stablecoin to have lower financial risk exposure, the reserve value should show positive and steady growth. Such trends in how the reserve value changes over time give information on the performance of the token in the market.

Collaterals (on-chain) – coefficient of variation of assets

The coefficient of variation is considered for the top 10 assets in the collateral pool for each stablecoin. For each asset, coefficient of variation is calculated by dividing the standard deviation of asset price by mean asset price in the past one year. Next, the coefficient of variation of the whole asset pool is calculated by summing the coefficients for each single asset, according to proportions of value.

CV=σ/μ

For example, the top components of DAI’s collateral pool are WETH, WBTC, USDC… etc. The coefficient of variation for DAI’s collateral pool will be the sum of the coefficient of variation of these assets. This metric gives information on the volatility of change in value of the reserve pool. Tokens with lower volatility will subsequently have lower level of financial risk exposures.

Collaterals (on-chain) – C-ratio

Another important aspect of collaterals are the collateralisation ratios, also known as c-ratios. Given the common issue for most on-chain assets of having considerably lower liquidity than off-chain assets due to high transaction cost and limited market sizes, the collateral ratio should be sufficiently above 100% to reduce the likelihood of mass liquidation during unexpected events, especially if the assets used as collaterals have high price volatility.

Although happening at very rare cases, it is also important to note if there are historical incidences where value of total collateral held by the protocol falls below the minimum required c-ratio. Such incidents hint that the protocol may have weaker financial ability to stand through a market downturn.

Collaterals (off-chain) – maturity date

An important feature about fiat assets is the maturity date. Here, we will stick with the commonly accepted definition of short term assets as assets with less than 90 days of maturity. A stablecoin has less financial risk exposures when a higher amount of reserve is made up of short term assets, which have higher liquidity and present value. In addition, since reserve value is often an estimated cashable value of the reserve, the estimated price of short term assets is also more reliable.

An area to look out for is that some protocols define the term short term assets differently as less than 120 days to maturity in their reserve attestation reports. Thus it is important to check details of maturity date, instead of just taking reported data on proportion of short term assets.

Collaterals (off-chain) – asset ratings

This section applies for all off-chain assets in the collateral pool that are not cash. Some common assets being used are short term corporate bills, bonds and fiduciary deposits. These assets should be at least an investment grade under the major credit rating systems like S&P and Fitch, so as to ensure the assets are unlikely to default and cause negative impact on the stablecoin’s reserve value. However, we have seen that a considerable number of protocols have not started releasing detailed information on asset ratings yet. But as the information disclosure requirements grow into a more standardised one, we can expect to know more about asset ratings in the future.

External regulation – regulation and holder of reserve accounts

In general, stablecoins face less financial risk exposures when they are faced with stricter regulations. Compliance to external regulations often require protocols to conduct frequent technical audits to ensure technical soundness of smart contracts, release regular and professional financial reports to disclose information on reserve and protocol financial performances. These actions would help protocols in better managing their financial operations, and prevent the loss of investor confidence due to information asymmetry.

The degree of regulation is especially important for analysing fiat based stablecoins, where value of the reserve pool is heavily dependent on how cash deposited by borrowers is being managed to back up its value. We have observed some protocols to be only registered under an entity without regulatory power, and misleadingly claim to be regulated. This is an area of precaution for investors. Alternatively, we can check on the management of the reserve pool to see which entity is holding and managing the collateral assets. For protocols that put cash in credible banks, the value of reserve is likely to be safe and insured against bank failures, but the passive style of management would make it vulnerable to macroeconomic changes like inflation. In cases of active management, the influence of macroeconomic changes is likely to be smaller, but there is a risk of incorrect management that brings instability to the reserve value.

Price reversion – efficiency of price balancing

One of the most important features, and the key to attract long term usage and holding, of stablecoins is to maintain prices at the pegged value. For stablecoins to have a lower level of financial risk exposures, prices should be able to return to target price quickly when it deviates away. Unlike the previous indicators that have been focusing on the price maintenance mechanism, this section focuses on empirical data and historical performance.

The efficiency of price balancing is measured using the price deviation metrics as explained in the previous articles. To recap, it is the percentage time where token price moved in a direction back to target price in the next time frame, given a deviation away from the target in the previous time frame. For a stablecoin to be considered having efficient price maintenance, this percentage should be as high as possible to show algorithm or reserve actions in place. There should also not be a distinct difference between price returning ability when price is above or below the target.

Calculating the scores

Based on the above indicators, a letter rating of A,B,C or D can be assigned by summing scores of all relevant sections, and comparing against the full applicable points. A general guideline is that tokens need be above 80% of the full score to be considered as rank A, above 70% for rank B, above 50% for rank C, and rank D for tokens with below 50% score.

We will demonstrate the rating system with an example of USDC. Being a stablecoin backed with fiat assets, USDC has been showing positive growth in reserve value of at a steady rate of 17% in average for the past year. Its reserve pool is 100% made up of credible short term assets, and regulated under strict supervision of 46 state regulators. It has an efficient price maintaining ability with price returning to target at 67% of times in Sept to Dec 2021. These give USDC a grade A ranking for financial risk exposures.

Upon conducting the similar procedure on a group of 18 stablecoins using data from Jan to Dec 2021, we get a list of risk ratings below.

Table 2. Risk ratings for 18 stablecoins in 2021

From the result, there is a distinction between the level of financial risk exposures for different types of stablecoins. Stablecoins backed with fiat assets have the least amount of financial risk exposures, potentially due to the stricter regulations that set higher requirements for the protocol’s financial structures. Next are stablecoins backed with on-chain assets, where over-collaterilisations provide a cushion for market wide financial downturns. Algorithmic stablecoins also face a generally high amount of financial risk, as the price balancing mechanisms often require active participation from the market to remain efficient.

Interpreting risk levels

This ratings system can be used to estimate the degree of market changes on protocol’s financial health and ability to maintain at pegged value. In general, stablecoins with higher letter grade (A) will subject to less financial risk exposures. The grades can be explained as followings.

A: Lowest level of financial risk exposures. Market changes are not expected to cause significant impact on the protocol’s financial structure and token’s ability in maintaining value.

B: Lower level of financial risk exposures. Market changes are not expected to cause significant impact on the protocol’s financial structure, but may disrupt the stablecoin’s ability to maintain price at pegged value for short periods of time.

C: High level of financial risk exposures. Protocol meets the basic financial requirements, but is vulnerable to market changes. Price is able to maintain at pegged value when the market is relatively stable.

D: Highest level of financial risk exposures. Protocol’s financial structure is highly vulnerable to market changes. Price is not maintained at pegged value even when the market is relatively stable.

Conclusion

With this system, we can now conduct cross-token financial risk comparisons between different stablecoins easily, and deduce the relative amount of financial risk exposures faced by each token. This would help investors in making important buying and selling decisions, especially in the long term. While the indicators used in this system may not be extensive, it considers the most essential components of financial risk, and investors can use it flexibly by adding or modifying any metrics to suit their needs.